As you approach your social security retirement age, your thoughts turn to deciding when you should begin receiving social security benefits. With over 2,700 rules in the social security manual, you’d be forgiven (and, for that matter, so would most social security case workers) for being bewildered and confused about all of the options available to claim social security. In this article, I attempt to distill the most frequently asked questions and help reduce confusion about claiming social security benefits (SSB).

The crux of this article is to discuss the advantages of planning the payout of your (or your spouse’s) benefits to maximize your ultimate financial payoff. Coordinating your benefits with your spouse’s benefits introduces complexities that must be understood to maximize your overall benefits. Combined with the ability to file for benefits, then suspend them or filing for benefits using your ex-spouse’s earnings records, planning for social security benefits can be quite complex.

I realize that, as a financial planner, it’s somewhat self-serving to say that each person’s situation is unique and requires a personalized and thorough analysis of the facts and circumstances to determine the optimal timeframe to claim SSB. Nonetheless, no article, however detailed, can take into account all individual situations.

Note that this article doesn’t attempt to discuss the viability of the social security system or whether benefits will be available in the future (I believe that they will be, perhaps on a somewhat reduced basis).

Social Security Basics

In general, if you’ve worked and sufficiently paid into the social security system for at least 40 quarters of work in your lifetime, you probably have some SSB coming to you when you retire. Calculation of the level of your benefit is quite complicated, but mostly affected by your lifetime earnings.

Even if you’ve never worked a day in your life, your spouse’s (or ex-spouse’s) earnings and qualifications may be your “ticket” to qualify for benefits. If you’ve earned little money in your lifetime (as is the case for a stay-at-home spouse), you can often qualify for a much higher benefit if you file based on your spouse’s (or ex-spouse’s) earnings.

There are three dates in which to begin drawing social security: early retirement age (ERA), full retirement age (FRA) and deferred retirement age (DRA), each one being a later date in life than the previous. Your ERA and FRA vary depending on your birthday, and are generally higher for younger retirees (for anyone born after 1959, their FRA is 67). For general discussion purposes, let’s assume that age 62, 67, and 70 are the ERA, FRA, and DRA respectively.

Deferring the date that you begin receiving benefits obviously means that you (and your spouse) may receive higher benefits per month until your date of death. Currently, less than 50% of filers wait until their FRA to claim benefits, and less than 6% wait until their DRA to claim benefits, despite the much higher DRA benefit (about 75% higher). The DRA benefit is generally about 30% higher than the FRA benefit. Reasons people cite for not deferring benefits include financial need, bad health, fear of social security insolvency, dying early, or plain ignorance about the overall benefits of waiting.

Once you begin receiving benefits, you may have options to suspend them within 12 months of starting them to qualify for a higher later benefit. This mostly involves repaying all of the benefits received. As more fully described below, there may be circumstances where you might want to file for SSB and immediately suspend them at FRA (without receiving payments) to allow your spouse to receive a higher (spousal) benefit or to receive a higher benefit at DRA.

Deferring Benefits

In general, deferring SSB as long as possible makes a lot of sense if you can afford to do so. The significant increase in benefits is primarily due to the additional years of compounding that occurs when you defer benefits.

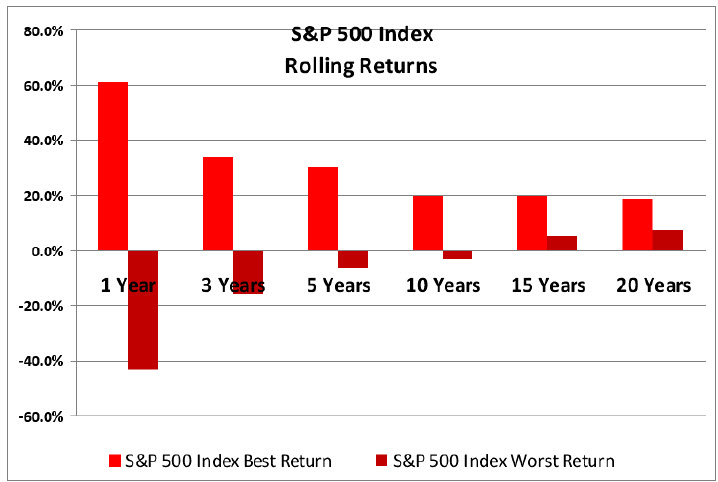

At its very core, social security is exactly like taking the sums that you contributed into the system over your working years and continuing to invest it. Just like any investment, the primary factors that affect the payout are the length of time for compounding and the rate of return applied. The longer you wait for benefits, the larger the invested sum grows.

Making a decision to begin or defer benefits is an exercise in making a best guess on how long you (and your spouse if you’re married) will live. “Gaming” social security is about maximizing the benefits you collect over your lifetime. Deciding to defer social security until age 70 is a losing proposition if you’re in bad health and don’t have much of a chance to make it to or much past that age. Conversely, if you’re healthy and your family has a past history of living well into their nineties, deferring benefits may or may not lead to a higher overall lifetime payout. Obviously, the “game” ends when you die, since your benefits cease then. So just like investing, the outcome of the decision to defer isn’t known until the investing and disbursement period is over.

Essential Rules/Facts

Given the forgoing background, here are some of the essential rules/facts to know about filing for SSB and some potential tax planning points:

1. At full retirement age (FRA), one may receive the higher of their own retirement benefit or a spousal benefit equal to 50% of their spouse’s retirement benefit. Many do not realize that in order to claim that spousal benefit, the spouse on whose record the 50% payment is based must be receiving or have filed for (and perhaps suspended) retirement benefits.

2. If a worker starts benefits prior to his/her FRA, and his/her spouse is receiving retirement benefits, the worker does not get to choose between their retirement benefit and a spousal benefit. They are automatically deemed to have begun their retirement benefit, and if their spouse is receiving retirement benefits, a supplement is added to reach the spousal benefit amount. All this is reduced for starting early. The total will be less than half the normal retirement benefit.If you start your retirement early and your spouse has not claimed or suspended his/her retirement benefit, you cannot get a spousal supplement until they do file.

3. A person needs to have been married to an ex-spouse for at least ten years immediately before a divorce is final, in order to be eligible to receive a spousal benefit based on a former spouse’s record. The ex-spouse need not approve this and may never know this is the benefit being claimed.If you marry again, you are no longer eligible for a spousal benefit on your ex’s record and a new 10-year clock starts on the marriage to your new spouse. If you are over 60 when you get married again, you will still be able to claim survivor benefits on your ex.

4. If you take your retirement early, it not only reduces your retirement benefits, benefits for your survivor (if any) are also based on that permanently reduced amount.

5. If you have claimed your retirement benefit early, when you reach your FRA, if your spouse then files for his/her retirement and you want to switch to a spousal benefit, you will not get 50 percent. The formula is (A-B) + C where A= ½ the worker’s Primary Insurance Amount (PIA, their benefit at their FRA), B= 100 percent of the spouse’s PIA, and C= the spouse’s EARLY retirement benefit. Since starting early means C is less than B, the total is less than 50%. One only gets half their spouse’s benefit if the spousal benefit is claimed at FRA.

6. Spousal benefits do not receive delayed credits. In other words, if taking the spousal benefit is good for a couple, delaying the claim for spousal benefits past the recipient’s FRA has no additional benefit. The same applies for widow/widower benefits. They can be started early but there is no benefit to delaying past FRA as no delayed credits apply. Before a worker dies, delaying does increase the potential survivor’s benefit.

7. Taxpayers whose income is low can find that some forms of tax planning can result in higher than expected taxation. Many retirees will make distributions from IRAs or qualified retirement plans prior to age 70½ to have a low tax rate applied. Roth conversions are often done for the same reason. A relatively small amount of taxable income can cause up to 85% of Social Security payments to become taxable.

8. Because the income thresholds that determine how much of one’s Social Security is taxable are not indexed for inflation, over time, more and more of the benefits can become taxable.

9. New this year, an increase in taxable income as just described can also cause a reduction or elimination of subsidies available to lower income households under the new health insurance law. Social Security payments, even the tax-exempt portions, are included in this evaluation. Supplemental Security Income (SSI) is excluded.

10. With today’s mobile workforce, it is not unusual to find some taxpayers that worked at a job and earned a pension benefit but were not subject to withholding for Social Security taxes and another job that was subject to Social Security taxes. Many such folks are unpleasantly surprised that their Social Security benefits may be reduced due to the Windfall Elimination Provision.

11. If you “file and suspend” for SSB, Medicare premiums cannot be paid automatically from Social Security income and must be paid directly to the Center for Medicare & Medicaid Services (CMS). Affected taxpayers should be sure to get billed properly by CMS. If it is not paid timely, you can lose your Medicare Part B coverage.

12. When collecting retirement benefits, increases in Medicare Part B premiums are capped to the same rate of increase of the retirement benefits under a “hold harmless” provision. This is tied to actual receipts so while delaying past your FRA earns delayed credits, there is no cap on the Medicare increases. Worse yet, the uncapped increase is locked into every future premium. This hold harmless quirk is not relevant to high income taxpayers. Hold harmless does not apply to high income taxpayers paying income-related Medicare B premiums.

13. Because it used to be allowable to pay back all of your retirement benefits and start over, many people think that they can change their minds about starting SSB early. Withdrawing your claim this way basically erased the claim as though it never happened and future benefits would therefore be higher. Today, if you regret your choice, you can only withdraw your claim and pay back benefits within 12 months of your early start. After 12 months, you are stuck with your choice until your FRA, at which point you can suspend and earn delayed credits up to age 70. The credits are applied to your reduced benefit.

Some Strategies and Conclusion

Here are some final considerations to make when deciding to file a claim for SSB (by necessity, these are generalities that must take into account each individual’s/couple’s facts and circumstances):

• Assess your own life expectancy, and, if married, your joint life expectancy.

• If married, and either spouse is healthy, delay the higher earner’s benefits as long as possible.

• If married and one spouse is unhealthy, get the lower payout as soon as possible.

• Supplement benefits with spousal amounts, if within FRA.

As mentioned above, the decision of when to file for social security benefits can become very complex and requires assessment of many factors. Since the determination can involve differences of thousands of dollars per person, per year, it’s worthwhile to carefully assess and model all of the facts and circumstances before starting benefits. Even though a total SSB re-do is no longer available, there are some options still available to modify benefit payouts.

It may be tempting or convenient to utilize a simplified web-based social security calculator to help you make an estimate, but be wary of any program that doesn’t model multiple scenarios or doesn’t require entry of many variables that may ultimately affect your optimum benefit. In the end, there’s no perfect answer, but perhaps a “best fit” for your situation is good enough.

If you have any questions about social security planning or any other financial planning matter, please don’t hesitate to contact me or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first.