Researchers have found that investors have a tendency to psychologically exaggerate declines in the performance of an investment and to minimize gains. It’s a phenomenon with a complex sounding name — “myopic loss aversion” — but also one that makes a simple point: Psychology plays a role in our investment decisions. Understanding that role, the subject of this second installment of a three-part series on investment risk, may help you stay on course toward your long-term financial objectives.

Word Play

Individuals subconsciously “frame” expectations based upon how the information is presented to them. For instance, would you prefer to invest in a security that has a 40% chance of yielding negative returns or one that has a 60% chance of yielding positive returns? Many people would choose the latter, even though the same investment opportunity was offered in both cases.

Running With the Pack

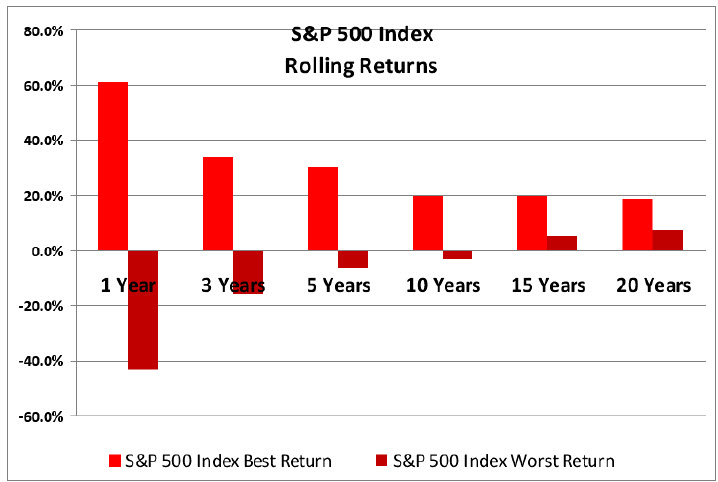

It’s human nature to want to choose investments that have performed well. On the other hand, many of us are naturally risk-averse. Sometimes these inclinations combine to make us less effective investors. For instance, do you know people who wait to invest until they hear of a security that consistently produces above-average returns? Then, sensing a “safe bet,” they purchase this investment — often when it’s at peak value. If the investment drops in value, they move their money to what they perceive as a less risky security or even pull out of the market altogether — even if such a move clashes with their long-term goals.

This sort of short-term thinking creates risk, too. When investors move in and out of the market, they’re practicing an investment tactic known as market timing. The risk is that they’ll mistime the market and lose out on potential gains. Even professional portfolio managers admit that it can be difficult to predict market moves.

Personal Experiences and Our Portfolios

Research has shown that individuals who grew up during the Great Depression are more likely to invest conservatively, while those who entered the market during the mid-1990s expect high returns and tend to invest more aggressively. Being aware of how past experience may influence your perceptions, can help you avoid financial strategies that may work against you.

So What Can You Do?

Several strategies may help you minimize the role that emotions and psychological tendencies play in your investment decisions. Stay focused on your long-term goals and not the market’s short-term moves. And rather than reviewing your investments’ performance every week, consider scheduling quarterly or semi annual portfolio reviews with a qualified financial professional.

Finally, develop — and stick to — a well thought out plan that’s based on your goals and your personal tolerance for risk. Look for more on these and other strategies that may help you cope with risk in the final installment of this series.

If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch.