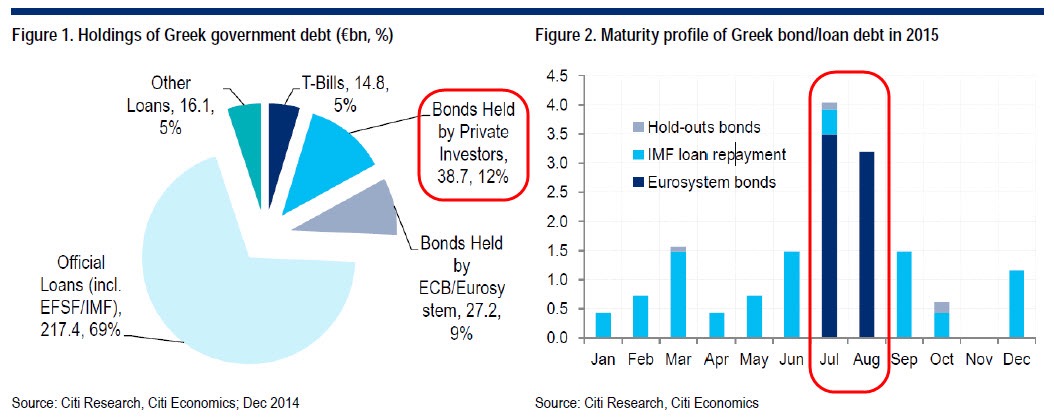

Any way you look at it, the standoff between the nation of Greece and the leaders of the European Union is a mess. But it may not be quite the problem that the press is making it out to be. In case you haven’t been following the story, the gist of it is that the Greek government, over a period of years that included the time it hosted the Summer Olympics, issued more bonds than, in retrospect, it could possibly pay back. The total debt outstanding peaked at somewhere around $340 billion, which is actually more than the $242 billion in goods and services that the entire Greek economy produces in a year. You’ve no doubt heard about a series of bailouts organized by the European Union, the International Monetary Fund and other groups which have collectively extended loans and extensions amounting to $217 billion to date. As you can see from Figure 2, on the right-hand side, roughly $4 billion in payments are due in July and more than $3 billion in August, after which time the payment schedule becomes somewhat more forgiving through 2022.  There are three problems with this picture. First, it has become apparent that Greece doesn’t have the money to make the July and August payments. Second, in return for additional debt relief, the various creditors are asking that the Greek government do more than just balance its budget (which it has). Their demands seem a bit harsh and somewhat picky when they’re organized in a list: Greece would have to reduce pension payments to current and retired workers by 40%, raise the retirement age to 67 in 2022 rather than 2025, phase out supplemental bonuses for poorer retirees in 2017 rather than 2018, and cut back on early retirement immediately. (The proposals also include additional taxes on consumers but not businesses.) And third: the newly-elected Greek government, led by Alexis Tsipras of the Syriza party, ran on a platform of rejecting any further budget concessions and compromises. This turned out to be an extremely successful political strategy: the party won 149 out of the 300 seats in the Greek Parliament in what is regarded as a rousing popular mandate. Negotiations predictably broke down, and now the Syriza leaders are asking the Greek citizens to vote on whether they will accept the or reject the austerity measures that the EU creditors are demanding. Polls suggest that the voters would like to keep their country in the Eurozone but that they oppose any additional budget reductions. In other words, nobody knows how the referendum will end. If the citizens of Greece reject austerity, it will present the European Union with a difficult choice: back down and continue to help Greece ease out of the crisis (which would be politically difficult to sell, especially to German voters), or deny the concessions that Greece needs, and effectively force Greece out of the Eurozone. If the latter happens, then the future becomes a bit murky. Greek banks have been shut down in advance of the July 5 vote, strongly suggesting that Greek leaders, holding a “no” vote, would no longer use the euro as its currency. They would print drachmas, which, in those frozen bank accounts, would replace euros at par. The drachmas would immediately lose value on the international markets, which would allow Greece to undercut its competitors in the export markets. Meanwhile, Greece could default on all or portions of its debt, and offer to pay drachmas instead. Who loses in this scenario? Everybody. The European banks holding Greek debt and private investors, are the obvious losers. But closer to home, any Greek citizen who didn’t get his/her money out of the bank before the freeze, will have to accept a haircut on the deposits, as drachmas will inevitably be worth less than euros. At the same time, many Greek banks are holding massive amounts of Greek government debt, which they need as collateral for European Central Bank loans that are keeping THEM (the banks) afloat. Alternatively, Greece could offer everyone 50-70 cents on the dollar in debt repayments, and would probably get mostly takers from creditors who would like to put this whole saga behind them. Do YOU lose in any of these scenarios? If either side blinks, then the situation goes back to business as usual. If Greek voters agree to give the EU what it wants, then some economists believe that the Greek economy will go into a steep recession, but your personal exposure to Greek companies is almost certainly minimal, and the problem will be temporary. If Greek voters vote “no”, the EU negotiators remain intractable and Greece leaves the Eurozone, then you can expect breathless and sometimes scary headlines and short-term turmoil in European stocks, with some investors panicking and others uncertain. But the smart money says that the Eurozone is strong enough to sustain the loss of one of its smallest economies, and Greece, too, will survive. The irony, which nobody seems to have noticed, is that after accepting many of the earlier austerity measures, the Greek government is actually running a budget surplus without the debt payments—something U.S. citizens can only dream of. If the additional austerity measures do, eventually, get put in place, the subsequent recession would reduce tax receipts and push Greece back into deficits again. If you’re a Greek citizen who hit the ATM after they had run out of money, then this is a pretty big crisis for your long-term financial situation. Otherwise, like most so-called “crises,” the possibility of a “Grexit” and the upcoming special election in Greece is more about entertainment than about making or losing money in your long-term portfolio. There may even be opportunities to buy some good solid companies or funds from those panicking out of their positions. So the Grexit is a non-issue for anyone not living and working in Greece. Our financial system had five years to manage, hedge, and otherwise reduce exposure to a Greek default. Most Greek debt is now held by European governments who can weather these losses. For them it isn’t a big deal because they didn’t enter into these positions expecting a profit, or even their money back. All they were doing is buying stability and time. And given that they delayed the inevitable Greek default by five years, they did a pretty good job. While a few politicians might lose their jobs and damage their legacy over this, the financial system will survive without Greece because of the time they bought us. If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch. Sources: https://en.wikipedia.org/wiki/Economy_of_Greece http://confluenceinvestment.com/assets/docs/2015/daily_Jun_29_2015.pdf http://www.zerohedge.com/news/2015-02-03/who-owns-greek-debt-and-when-it-due http://www.washingtonpost.com/blogs/wonkblog/wp/2015/06/25/europe-strikes-back-it-seems-to-be-trying-to-push-greece-out-of-the-euro/ TheMoneyGeek thanks guest writer Bob Veres for his help writing this post

There are three problems with this picture. First, it has become apparent that Greece doesn’t have the money to make the July and August payments. Second, in return for additional debt relief, the various creditors are asking that the Greek government do more than just balance its budget (which it has). Their demands seem a bit harsh and somewhat picky when they’re organized in a list: Greece would have to reduce pension payments to current and retired workers by 40%, raise the retirement age to 67 in 2022 rather than 2025, phase out supplemental bonuses for poorer retirees in 2017 rather than 2018, and cut back on early retirement immediately. (The proposals also include additional taxes on consumers but not businesses.) And third: the newly-elected Greek government, led by Alexis Tsipras of the Syriza party, ran on a platform of rejecting any further budget concessions and compromises. This turned out to be an extremely successful political strategy: the party won 149 out of the 300 seats in the Greek Parliament in what is regarded as a rousing popular mandate. Negotiations predictably broke down, and now the Syriza leaders are asking the Greek citizens to vote on whether they will accept the or reject the austerity measures that the EU creditors are demanding. Polls suggest that the voters would like to keep their country in the Eurozone but that they oppose any additional budget reductions. In other words, nobody knows how the referendum will end. If the citizens of Greece reject austerity, it will present the European Union with a difficult choice: back down and continue to help Greece ease out of the crisis (which would be politically difficult to sell, especially to German voters), or deny the concessions that Greece needs, and effectively force Greece out of the Eurozone. If the latter happens, then the future becomes a bit murky. Greek banks have been shut down in advance of the July 5 vote, strongly suggesting that Greek leaders, holding a “no” vote, would no longer use the euro as its currency. They would print drachmas, which, in those frozen bank accounts, would replace euros at par. The drachmas would immediately lose value on the international markets, which would allow Greece to undercut its competitors in the export markets. Meanwhile, Greece could default on all or portions of its debt, and offer to pay drachmas instead. Who loses in this scenario? Everybody. The European banks holding Greek debt and private investors, are the obvious losers. But closer to home, any Greek citizen who didn’t get his/her money out of the bank before the freeze, will have to accept a haircut on the deposits, as drachmas will inevitably be worth less than euros. At the same time, many Greek banks are holding massive amounts of Greek government debt, which they need as collateral for European Central Bank loans that are keeping THEM (the banks) afloat. Alternatively, Greece could offer everyone 50-70 cents on the dollar in debt repayments, and would probably get mostly takers from creditors who would like to put this whole saga behind them. Do YOU lose in any of these scenarios? If either side blinks, then the situation goes back to business as usual. If Greek voters agree to give the EU what it wants, then some economists believe that the Greek economy will go into a steep recession, but your personal exposure to Greek companies is almost certainly minimal, and the problem will be temporary. If Greek voters vote “no”, the EU negotiators remain intractable and Greece leaves the Eurozone, then you can expect breathless and sometimes scary headlines and short-term turmoil in European stocks, with some investors panicking and others uncertain. But the smart money says that the Eurozone is strong enough to sustain the loss of one of its smallest economies, and Greece, too, will survive. The irony, which nobody seems to have noticed, is that after accepting many of the earlier austerity measures, the Greek government is actually running a budget surplus without the debt payments—something U.S. citizens can only dream of. If the additional austerity measures do, eventually, get put in place, the subsequent recession would reduce tax receipts and push Greece back into deficits again. If you’re a Greek citizen who hit the ATM after they had run out of money, then this is a pretty big crisis for your long-term financial situation. Otherwise, like most so-called “crises,” the possibility of a “Grexit” and the upcoming special election in Greece is more about entertainment than about making or losing money in your long-term portfolio. There may even be opportunities to buy some good solid companies or funds from those panicking out of their positions. So the Grexit is a non-issue for anyone not living and working in Greece. Our financial system had five years to manage, hedge, and otherwise reduce exposure to a Greek default. Most Greek debt is now held by European governments who can weather these losses. For them it isn’t a big deal because they didn’t enter into these positions expecting a profit, or even their money back. All they were doing is buying stability and time. And given that they delayed the inevitable Greek default by five years, they did a pretty good job. While a few politicians might lose their jobs and damage their legacy over this, the financial system will survive without Greece because of the time they bought us. If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch. Sources: https://en.wikipedia.org/wiki/Economy_of_Greece http://confluenceinvestment.com/assets/docs/2015/daily_Jun_29_2015.pdf http://www.zerohedge.com/news/2015-02-03/who-owns-greek-debt-and-when-it-due http://www.washingtonpost.com/blogs/wonkblog/wp/2015/06/25/europe-strikes-back-it-seems-to-be-trying-to-push-greece-out-of-the-euro/ TheMoneyGeek thanks guest writer Bob Veres for his help writing this post

“Grexit” Vote Coming

June 30, 2015 — Sam H. FawazThe Value of Objective Financial Planning

June 23, 2015 — Sam H. FawazWhat is the value that people get when they work with an objective, client-focused financial planner?

Most planning firms are reluctant to toot their own horns—partly out of modesty, and partly out of a conviction that you probably have better things to do than read about how they help you with your financial life. But every once in a while, it’s a good idea to stop and think about what you get, for what you pay.

This list is organized in rough order of value, and if you feel you aren’t getting all of these benefits from your financial planner, you should let her or him know.

1) An independent financial planner helps protect you from financial predators.

It’s a touchy issue in the profession whether advisors who put their clients’ interests first should be “bashing the competition,” but in fact the Wall Street firms that pretend to offer financial planning guidance are seldom (if ever) looking out for the best interests of their customers. When you work with a broker (possibly also known, on their business card, as “vice president of investments,”) you will be presented with separately-managed accounts that look like mutual funds, except they share their fees with the brokerage firm, plus a lot of investments that have to pay people to recommend them—never a good sign for the end investor.

And since the investment markets are extremely complicated, it’s usually hard for a layperson to know when there are much better alternatives than the “opportunities” being presented.

2) An independent financial planner helps you keep track of and make your financial affairs more efficient.

It is not uncommon for financial planners to talk with clients who once had a will drawn up, but they’re not sure exactly when. Now that you mention it, they’re curious about what, exactly, it says. There’s a life insurance policy in a drawer somewhere, and it may be a term policy or it may be a cash value contract; all the client knows for sure is that she writes a check to the insurance company every year. Upon inspection, it turns out the auto insurance policy she happens to own is way more expensive than the lowest rate available in the market, and the homeowner’s policy hasn’t been updated since the Clinton Administration.

And the investments are not uncommonly a hodgepodge of what a broker sold the client based on what he was told by his bosses to recommend at different times during the relationship.

Hopefully, this was never you. But it does offer a certain peace of mind to know that everything is organized, in one place, and that somebody is paying attention to the details. Because in your financial life, the details matter.

3) An independent financial planner will stand between his/her clients and the dysfunctional emotional decisions that everybody makes with their own investments.

Do you remember how it felt when Lehman Brothers went down, and the U.S. government was bailing out General Motors? Many people sold everything at the bottom, and then waited, and waited, and waited to get back into the markets until it was “safe.” To this day, I still get calls from people who left the markets near the bottom and never got back in. They never dreamed that the markets would go on six year bull run that would take us to new record highs, and want to know if it’s too late to get back in.

The Morningstar (research) organization has calculated the difference between investment returns and investor returns—that is, between the returns people actually get vs. what the markets (or individual mutual funds) have delivered. Results? It is not unusual, during various time periods, for individual investors to get about half the returns of the market. How is that possible? They may be moving the portfolio around, or buying an attractive-looking hot fund or selling a great fund that’s going through a rough patch. They may sell out at the bottom of a scary period, or go all-in when the markets are about to take a nasty tumble.

For many of us, the best approach is to find good, solid investments and stay the course through thick and thin, ups and downs. But it’s very hard to do those things on your own. An independent advisor provides a dose of objectivity right when you need it.

4) An independent financial planner is a strong advocate for your future.

You know the statistics about the savings rate in America (the 2000-2008 numbers hovered around 0% of income, spiked briefly after the Great Recession, and are now back in the 1% range again). But the keepers of these statistics don’t tell you that they probably overstated the actual rate, because they didn’t include things like increasing credit card balances or home equity loans. When people put money in their savings account, and at the same time run up more debt, they still counted it as an increase in their savings.

The problem for most consumers is that there is no voice in their environment advising them to pay themselves a fair percentage of the income that they earn. Instead, they’re bombarded by messages which make powerful arguments to do the opposite: to buy this, that, or something else. The entire advertising community conspires to take those dollars out of their hands before they ever hit an investment account.

Advisors become that rare voice speaking out in favor of saving. And in some cases, they help identify expenditures that are not in line with your stated future goals. Which leads us to:

5) An independent financial planner helps people identify what is important in their lives and prioritize their goals.

How many people do you know who have taken the time to identify what they really want out of life?

The incredibly sad truth is that the vast majority of people in our advanced, prosperous society have not taken the time to figure out what they really want out of the all-too-brief time they will spend on this planet. And because they don’t know their destination, they will never reach it. They are, in a very real sense, at the mercy of whatever agenda others have for them.

An independent financial planner will ask questions in your initial interview which help you recognize what you don’t know about what you want, and help you identify your most personal goals and desires. That, alone, can be a priceless service.

6) An independent financial planner can help people turn seemingly impossible goals into a routine that can achieve them.

After years of running retirement planning spreadsheets, and working with successful individuals in the community, advisors eventually master one of the truly magical lessons of life: that any enormous goal can be broken down into manageable, monthly increments, and achieved by routine and persistence. You save X amount of dollars every month in a portfolio that gets something close to what the market offers, and you will retire with a sum of money that seems impossible to you now.

Clients who have goals that they don’t believe they can achieve are put on a schedule that will get them there as a matter of routine.

Of course, this list doesn’t include specialized services like making retirement planning projections, charitable planning, creating special needs trusts for a disabled child, reducing overall taxes, social security planning, evaluating disability and long-term care insurance—and it doesn’t mention the comfortable knowledge that you can call an expert for advice on virtually any financial subject, and you’ll get an answer that is not tainted by a sales agenda.

The point is that the services offered by an independent financial planner can have enormous value to people who are motivated to enjoy successful, prosperous lives. An independent planner’s only goal is your success and prosperity, which should not be—but is—unusual in our financial world.

If you would like to review your current investment portfolio or discuss possibly hiring us as your financial planner, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch.

TheMoneyGeek thanks guest writer Bob Veres for contributing to this post

It’s 2015: Do You Know Who Your Beneficiaries Are?

June 7, 2015 — Sam H. FawazMany IRA owners may not be aware that after their death, the primary beneficiary — usually the surviving spouse — may have the right to transfer part or all of the IRA assets into another account.

Many investors have taken advantage of pretax contributions to their company’s employer-sponsored retirement plan and/or make annual contributions to an IRA. If you participate in a qualified plan program you may be overlooking an important housekeeping issue: beneficiary designations.

An improper designation could make life difficult for your family in the event of your untimely death by putting assets out of reach of those you had hoped to provide for and possibly increasing their tax burdens. Further, if you have switched jobs, become a new parent, been divorced, or survived a spouse or even a child, your current beneficiary designations may need to be updated.

Consider the “What Ifs”

In the heat of divorce proceedings, for example, the task of revising one’s beneficiary designations has been known to fall through the cracks. While a court decree that ends a marriage does terminate the provisions of a will that would otherwise leave estate proceeds to a now-former spouse, it does not automatically revise that former spouse’s beneficiary status on separate documents such as employer-sponsored retirement accounts and IRAs.

Many IRA owners may not be aware that after their death, the primary beneficiary — usually the surviving spouse — may have the right to transfer part or all of the IRA assets into another account. Take the case of the IRA owner who has children from a previous marriage. If, after the owner’s death, the surviving spouse moved those assets into his or her own IRA and named his or her biological children as beneficiaries, the original IRA owner’s children could legally be shut out of any benefits.

Also keep in mind that the law requires that a spouse be the primary beneficiary of a 401(k) or a profit-sharing account unless he/she waives that right in writing. A waiver may make sense in a second marriage — if a new spouse is already financially set or if children from a first marriage are more likely to need the money. Single people can name whomever they choose. And non-spouse beneficiaries are now eligible for a tax-free transfer to an IRA.

The IRS has also issued regulations that dramatically simplify the way certain distributions affect IRA owners and their beneficiaries. Consult your tax advisor on how these rule changes may affect your situation.

To Simplify, Consolidate

Elsewhere, in today’s workplace, it is not uncommon to switch employers every few years. If you have changed jobs and left your assets in your former employers’ plans, you may want to consider moving these assets into a rollover IRA. Consolidating multiple retirement plans into a single tax-advantaged account can make it easier to track your investment performance and streamline your records, including beneficiary designations.

Review Your Current Situation

If you are currently contributing to an employer-sponsored retirement plan and/or an IRA, contact your benefits administrator — or, in the case of the IRA, the financial institution — and request to review your current beneficiary designations. You may want to do this with the help of your tax advisor or estate planning professional to ensure that these documents are in synch with other aspects of your estate plan. Ask your estate planner/attorney about the proper use of such terms as “per stirpes” and “per capita” as well as about the proper use of trusts to achieve certain estate planning goals. Your planning professional can help you focus on many important issues, including percentage breakdowns, especially when minor children and those with special needs are involved.

Finally, be sure to keep copies of all your designation forms in a safe place and let family members know where they can be found.

This communication is not intended to be tax or legal advice and should not be treated as such. Each individual’s situation is different. If you would like to review your current beneficiary designations or discuss any other estate or financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch.

Planning for Known — and Unknown — Health Care Costs in Retirement

June 1, 2015 — Sam H. FawazThe issue of health care costs in retirement — and planning for them well in advance of retirement — is becoming a centerpiece of any retirement planning discussion.

A recent study by Employee Benefit Research Institute (EBRI) projected that in 2014, men and women who wanted a 90% chance of having enough money to cover out-of-pocket health care expenses in retirement would need to have saved $116,000 and $131,000 respectively by age 65.1 This is a sobering goal when you consider that just 42% of workers in their 50s and 60s report total savings and investments in excess of $100,000.2

Part of the problem with putting a price tag on retiree health care expenses is that every situation will vary depending on an individual’s health, the type of health care coverage they carry, and when they hope to retire. That said, EBRI has identified some “recurring expenses,” or standard elements of cost that can be estimated and planned for in advance as well as “non-recurring” expenses that are less predictable but tend to increase with age.

Recurring vs. Non-Recurring Expenses

Using data gleaned from the Health and Retirement Study (HRS) — a longstanding, highly respected study of representative U.S. households with individuals over age 50 — EBRI was able to categorize utilization patterns and expenses for two separate types of health care services:

- Recurring services — include doctor visits, prescription drug usage, and dentist services. Since these services tend to remain stable throughout retirement, it is possible to calculate an average out-of-pocket expense among individuals age 65 and older of $1,885 annually.3 Projecting forward, and factoring in the following assumptions: a 2% inflation rate, a 3% rate of return on investments, and a life expectancy of 90 years, EBRI estimates that one would need $40,798 at age 65 to cover the average out-of-pocket expenses for recurring health care needs throughout retirement. It should be noted that this calculation does not include expenses for any insurance premiums or over-the-counter medications.

- Non-recurring expenses — include overnight hospital stays, overnight nursing home stays, home health care, outpatient surgery, and special facilities. Unlike recurring expenses, the cost of most non-recurring services increases with age. For example, average annual out-of-pocket expenses for nursing home stays are estimated at $8,902 for those in the 65 to 74 age group, $16,948 for those aged 75 to 84, and $24,185 for individuals aged 85 and up.3

Yet because the likelihood of utilizing these services and the degree to which they will be needed is largely unknown, projecting the savings needed to cover these costs throughout retirement is an elusive exercise. However, by thinking about the total out-of-pocket savings goals of $116,000 for men and $131,000 for women cited earlier in terms of recurring and non-recurring costs may help retirees and those nearing retirement in their planning efforts.

Bigger Picture Planning

As financial planners, we often recommend taking a holistic approach to calculating income needs in retirement, factoring in such costs as taxes and debt payments along with other typical expenses including health care. In addition to the out-of-pocket health care calculations discussed above, consider what you think you might have to pay in annual premiums if you were to apply for health insurance today. Lastly, and perhaps most important, add in an allowance for inflation — both general and health care inflation.

Your financial planner can help get the retirement income planning discussion started and — as part of that exercise — can work with you to put some numbers around your health care planning needs.

This article offers only an outline; it is not a definitive guide to all possible consequences and implications of any specific saving or investment strategy. If you would like to review your retirement plan, investment strategy or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch.

Sources:

1Employee Benefit Research Institute, news release, “Needed Savings for Health Care in Retirement Continue to Fall,” October 28, 2014.

2Employee Benefit Research Institute, 2014 Retirement Confidence Survey, March 2014. (Not including the value of a primary residence or defined benefit plans.)

3Employee Benefit Research Institute, “Utilization Patterns and Out-of-Pocket Expenses for Different Health Care Services Among American Retirees,” February 2015.