Since the beginning of last September, the stock markets have enjoyed a nearly uninterrupted bull uptrend which has been unprecedented in market history. Fueled by improving economics and Federal Reserve actions, the uptrend has withstood many geopolitical, fiscal and news driven setbacks. But today the political unrest in the Middle East, issues with Spanish debt repayment and a higher than expected weekly first-time unemployment claim number (497,000) were the 1-2-3 punch that the markets could not recover from and therefore we suffered a 1.5-2.5% setback. Be it stocks, gold, silver or oil today, they were all down today.

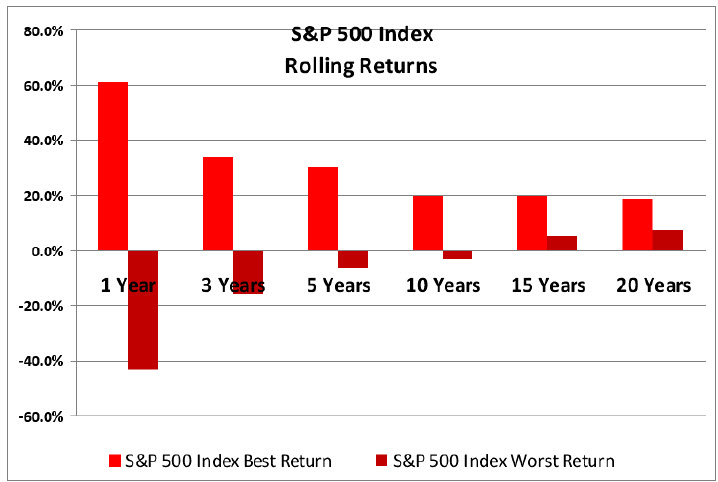

Normally, up-trending bull markets such as the one we’re in take rest periods, or “corrections” as they’re called, every couple of months while individuals and institutions take profits on stock positions and reset stock prices back to normal levels. Corrections (usually 10-20% of an index value such as the S&P 500) are healthy for the market and while uncomfortable if you watch them unfold from day to day, allow the markets to set up for the next leg up. Two years to the day yesterday into this bull run have seen us move up about 100% from the March 9, 2009 lows on the S&P 500 index. Without a doubt, this has been an incredible run and I hope you’ve been participating.

As I’ve discussed with clients and prospects recently, a correction in the market has been long overdue and anticipated. While today was the first big down day where we really tested key levels in the indexes, there have been several signs of exhaustion in the market. Despite this, I cannot say with certainty whether we’ve definitively entered into a correction period (technically we have, but it needs to be confirmed with follow-through on Friday and next week.) If the bulls get their act together tomorrow and “rescue” the market by pushing it back up through heavy volume buying, then this decline may be “all she wrote.” If not, we could head down to test the 1275 level of the S&P 500 index (we closed at 1295 today). A failure to hold the 1275 level means that large institutions have decided to continue selling and a drop to 1240 may need to exhaust sellers.

With the “Day of Rage” demonstrations scheduled for Friday in Saudi Arabia, rocketing oil prices and sovereign debt issues, the odds of avoiding a deeper correction are not very high. Besides, this correction is long overdue and may occur regardless of how peacefully the Middle East situation is resolved or even if oil prices come back down to earth.

What do I think? As I’ve mentioned before, the Federal Reserve has made investing in anything but the stock market earn near zero returns. That is, the government wants us to buy equities, push the stock market (and IRA’s and 401(k)’s) higher, to make us feel richer and more confident and therefore spend more. Spending more creates demand which in turn creates jobs and so on. So I believe that the gentle (if somewhat invisible) hand will come in to help support the market and avoid a protracted decline that might scare off the latest entrants into the market. While my crystal ball is still in the shop, I believe that a decline beyond 1275 in the S&P 500 (another 1.5%) is a stretch. While that would make it a very shallow correction, it may be enough to breathe new life into the stock market and help resume the uptrend.

So what should you do now in light of a possible correction? Basically, you shouldn’t do much if anything since nothing is confirmed. If you’re investing on your own, trying to time your “in’s and out’s” of the markets is nearly impossible and not recommended unless you’re an experienced trader. If you have a profitable position and worry about it turning into a loss, you may decide to sell a portion or all of it. More savvy investors may be able to hedge their positions with options or inverse ETF’s if the decline proves to be protracted. From our end for our clients, I’m watching the market technical levels on a daily basis like a hawk and already have begun to harvest some profits and protect some positions. If a protracted downturn does materialize, I may also hedge portfolios with inverse ETF’s and selectively liquidate partial positions. But we’re not there yet and I’m not making any recommendations. And by no means do I think we’re entering another bear market (by definition, a bear market begins when we decline 20% from the last peak in a major index). Non-clients should consult their current advisor (or me) if you’re unsure what to do in the event of a protracted decline and should not treat this as a recommendation to buy or sell anything (see disclaimer below).

Last year we declined nearly 15% from May through August amid sovereign debt worries and economic uncertainty and then proceeded to push up nearly 25% over the next six months. I still believe that we will end 2011 with double-digit gains in the markets as this economy matures from recovery to expansion. All economic indicators point positively and last month we even added nearly 200,000 new jobs. We may even see housing perk up a bit later this year. Without a doubt, sustained oil prices above $125 per barrel and $4 gasoline for an extended period (6 months or more), will put a crimp into the expansion, but I don’t believe we’re heading for a long term spike in oil prices. Let’s just say that the oil producing countries learned what supply constraints and speculation did to oil demand the last time oil spiked to $145 a barrel. More electric and hybrid cars is just one example of how we are learning to live with less demand for foreign oil.

I hope this message helps alleviate any anxiety over the recent down days in the market. Remember that the media loves good negative stories to help sell newspapers and advertising. Avoid the noise and try to keep your sanity during the days when it seems like there’s always something bad going on in the world. Middle Eastern concerns have been a worry for decades, if not centuries now, and likely won’t be resolved during our lifetimes. Like every other world incident, the markets get back to normal and we get through them.

Enjoy the upcoming weekend and don’t hesitate to contact me if I can be of any help. If you’re not a client, your consultation with me is complimentary, no-pressure and with no obligation. I’d love to talk to you whether or not you’re considering hiring a financial planner or money manager.

Sam H. Fawaz CFP®, CPA is president of YDream Financial Services, Inc., a registered investment advisor. Sam is a Certified Financial Planner (CFP®), Certified Public Accountant and registered member of the National Association of Personal Financial Advisors (NAPFA) fee-only financial planner group. Sam has expertise in many areas of personal finance and wealth management and has always been fascinated with the role of money in society. Helping others prosper and succeed has been Sam’s mission since he decided to dedicate his life to financial planning. He specializes in entrepreneurs, professionals, company executives and their families.

All material presented herein is believed to be reliable, but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment advisors before making any investment decisions. Opinions expressed in this writing by Sam H. Fawaz are his own, may change without prior notice and should not be relied upon as a basis for making investment or planning decisions. No person can accurately forecast or call a market top or bottom, so forward looking statements should be discounted and not relied upon as a basis for investing or trading decisions. This message was authored by Sam H. Fawaz CPA, CFP and is provided by YDream Financial Services, Inc.

My no-nonsense no-spam policy: If you’d prefer not to receive future updates, just reply and let me know by typing “unsubscribe” in the subject (please don’t hit the spam button-it just puts me on a universal spammer’s list which is tough to get off of.)I’ll take you off my list immediately and permanently. I will never sell, share, rent or give away your e-mail address to anyone. Period.