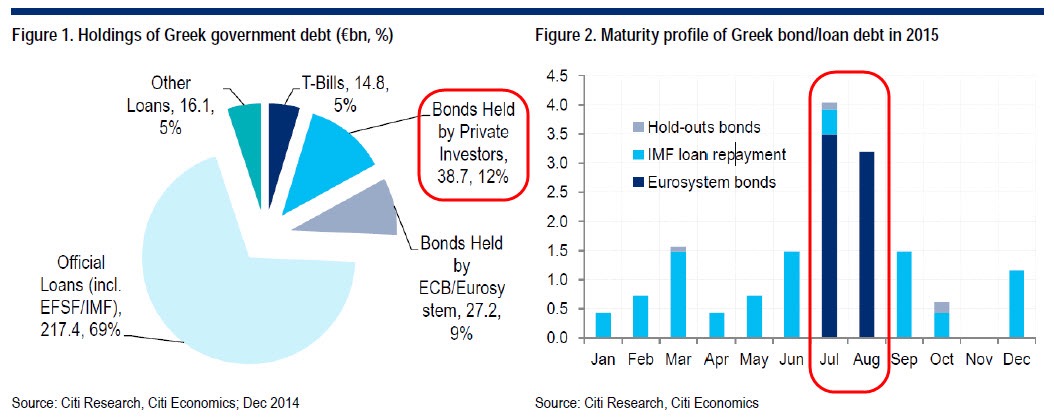

Any way you look at it, the standoff between the nation of Greece and the leaders of the European Union is a mess. But it may not be quite the problem that the press is making it out to be. In case you haven’t been following the story, the gist of it is that the Greek government, over a period of years that included the time it hosted the Summer Olympics, issued more bonds than, in retrospect, it could possibly pay back. The total debt outstanding peaked at somewhere around $340 billion, which is actually more than the $242 billion in goods and services that the entire Greek economy produces in a year. You’ve no doubt heard about a series of bailouts organized by the European Union, the International Monetary Fund and other groups which have collectively extended loans and extensions amounting to $217 billion to date. As you can see from Figure 2, on the right-hand side, roughly $4 billion in payments are due in July and more than $3 billion in August, after which time the payment schedule becomes somewhat more forgiving through 2022.  There are three problems with this picture. First, it has become apparent that Greece doesn’t have the money to make the July and August payments. Second, in return for additional debt relief, the various creditors are asking that the Greek government do more than just balance its budget (which it has). Their demands seem a bit harsh and somewhat picky when they’re organized in a list: Greece would have to reduce pension payments to current and retired workers by 40%, raise the retirement age to 67 in 2022 rather than 2025, phase out supplemental bonuses for poorer retirees in 2017 rather than 2018, and cut back on early retirement immediately. (The proposals also include additional taxes on consumers but not businesses.) And third: the newly-elected Greek government, led by Alexis Tsipras of the Syriza party, ran on a platform of rejecting any further budget concessions and compromises. This turned out to be an extremely successful political strategy: the party won 149 out of the 300 seats in the Greek Parliament in what is regarded as a rousing popular mandate. Negotiations predictably broke down, and now the Syriza leaders are asking the Greek citizens to vote on whether they will accept the or reject the austerity measures that the EU creditors are demanding. Polls suggest that the voters would like to keep their country in the Eurozone but that they oppose any additional budget reductions. In other words, nobody knows how the referendum will end. If the citizens of Greece reject austerity, it will present the European Union with a difficult choice: back down and continue to help Greece ease out of the crisis (which would be politically difficult to sell, especially to German voters), or deny the concessions that Greece needs, and effectively force Greece out of the Eurozone. If the latter happens, then the future becomes a bit murky. Greek banks have been shut down in advance of the July 5 vote, strongly suggesting that Greek leaders, holding a “no” vote, would no longer use the euro as its currency. They would print drachmas, which, in those frozen bank accounts, would replace euros at par. The drachmas would immediately lose value on the international markets, which would allow Greece to undercut its competitors in the export markets. Meanwhile, Greece could default on all or portions of its debt, and offer to pay drachmas instead. Who loses in this scenario? Everybody. The European banks holding Greek debt and private investors, are the obvious losers. But closer to home, any Greek citizen who didn’t get his/her money out of the bank before the freeze, will have to accept a haircut on the deposits, as drachmas will inevitably be worth less than euros. At the same time, many Greek banks are holding massive amounts of Greek government debt, which they need as collateral for European Central Bank loans that are keeping THEM (the banks) afloat. Alternatively, Greece could offer everyone 50-70 cents on the dollar in debt repayments, and would probably get mostly takers from creditors who would like to put this whole saga behind them. Do YOU lose in any of these scenarios? If either side blinks, then the situation goes back to business as usual. If Greek voters agree to give the EU what it wants, then some economists believe that the Greek economy will go into a steep recession, but your personal exposure to Greek companies is almost certainly minimal, and the problem will be temporary. If Greek voters vote “no”, the EU negotiators remain intractable and Greece leaves the Eurozone, then you can expect breathless and sometimes scary headlines and short-term turmoil in European stocks, with some investors panicking and others uncertain. But the smart money says that the Eurozone is strong enough to sustain the loss of one of its smallest economies, and Greece, too, will survive. The irony, which nobody seems to have noticed, is that after accepting many of the earlier austerity measures, the Greek government is actually running a budget surplus without the debt payments—something U.S. citizens can only dream of. If the additional austerity measures do, eventually, get put in place, the subsequent recession would reduce tax receipts and push Greece back into deficits again. If you’re a Greek citizen who hit the ATM after they had run out of money, then this is a pretty big crisis for your long-term financial situation. Otherwise, like most so-called “crises,” the possibility of a “Grexit” and the upcoming special election in Greece is more about entertainment than about making or losing money in your long-term portfolio. There may even be opportunities to buy some good solid companies or funds from those panicking out of their positions. So the Grexit is a non-issue for anyone not living and working in Greece. Our financial system had five years to manage, hedge, and otherwise reduce exposure to a Greek default. Most Greek debt is now held by European governments who can weather these losses. For them it isn’t a big deal because they didn’t enter into these positions expecting a profit, or even their money back. All they were doing is buying stability and time. And given that they delayed the inevitable Greek default by five years, they did a pretty good job. While a few politicians might lose their jobs and damage their legacy over this, the financial system will survive without Greece because of the time they bought us. If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch. Sources: https://en.wikipedia.org/wiki/Economy_of_Greece http://confluenceinvestment.com/assets/docs/2015/daily_Jun_29_2015.pdf http://www.zerohedge.com/news/2015-02-03/who-owns-greek-debt-and-when-it-due http://www.washingtonpost.com/blogs/wonkblog/wp/2015/06/25/europe-strikes-back-it-seems-to-be-trying-to-push-greece-out-of-the-euro/ TheMoneyGeek thanks guest writer Bob Veres for his help writing this post

There are three problems with this picture. First, it has become apparent that Greece doesn’t have the money to make the July and August payments. Second, in return for additional debt relief, the various creditors are asking that the Greek government do more than just balance its budget (which it has). Their demands seem a bit harsh and somewhat picky when they’re organized in a list: Greece would have to reduce pension payments to current and retired workers by 40%, raise the retirement age to 67 in 2022 rather than 2025, phase out supplemental bonuses for poorer retirees in 2017 rather than 2018, and cut back on early retirement immediately. (The proposals also include additional taxes on consumers but not businesses.) And third: the newly-elected Greek government, led by Alexis Tsipras of the Syriza party, ran on a platform of rejecting any further budget concessions and compromises. This turned out to be an extremely successful political strategy: the party won 149 out of the 300 seats in the Greek Parliament in what is regarded as a rousing popular mandate. Negotiations predictably broke down, and now the Syriza leaders are asking the Greek citizens to vote on whether they will accept the or reject the austerity measures that the EU creditors are demanding. Polls suggest that the voters would like to keep their country in the Eurozone but that they oppose any additional budget reductions. In other words, nobody knows how the referendum will end. If the citizens of Greece reject austerity, it will present the European Union with a difficult choice: back down and continue to help Greece ease out of the crisis (which would be politically difficult to sell, especially to German voters), or deny the concessions that Greece needs, and effectively force Greece out of the Eurozone. If the latter happens, then the future becomes a bit murky. Greek banks have been shut down in advance of the July 5 vote, strongly suggesting that Greek leaders, holding a “no” vote, would no longer use the euro as its currency. They would print drachmas, which, in those frozen bank accounts, would replace euros at par. The drachmas would immediately lose value on the international markets, which would allow Greece to undercut its competitors in the export markets. Meanwhile, Greece could default on all or portions of its debt, and offer to pay drachmas instead. Who loses in this scenario? Everybody. The European banks holding Greek debt and private investors, are the obvious losers. But closer to home, any Greek citizen who didn’t get his/her money out of the bank before the freeze, will have to accept a haircut on the deposits, as drachmas will inevitably be worth less than euros. At the same time, many Greek banks are holding massive amounts of Greek government debt, which they need as collateral for European Central Bank loans that are keeping THEM (the banks) afloat. Alternatively, Greece could offer everyone 50-70 cents on the dollar in debt repayments, and would probably get mostly takers from creditors who would like to put this whole saga behind them. Do YOU lose in any of these scenarios? If either side blinks, then the situation goes back to business as usual. If Greek voters agree to give the EU what it wants, then some economists believe that the Greek economy will go into a steep recession, but your personal exposure to Greek companies is almost certainly minimal, and the problem will be temporary. If Greek voters vote “no”, the EU negotiators remain intractable and Greece leaves the Eurozone, then you can expect breathless and sometimes scary headlines and short-term turmoil in European stocks, with some investors panicking and others uncertain. But the smart money says that the Eurozone is strong enough to sustain the loss of one of its smallest economies, and Greece, too, will survive. The irony, which nobody seems to have noticed, is that after accepting many of the earlier austerity measures, the Greek government is actually running a budget surplus without the debt payments—something U.S. citizens can only dream of. If the additional austerity measures do, eventually, get put in place, the subsequent recession would reduce tax receipts and push Greece back into deficits again. If you’re a Greek citizen who hit the ATM after they had run out of money, then this is a pretty big crisis for your long-term financial situation. Otherwise, like most so-called “crises,” the possibility of a “Grexit” and the upcoming special election in Greece is more about entertainment than about making or losing money in your long-term portfolio. There may even be opportunities to buy some good solid companies or funds from those panicking out of their positions. So the Grexit is a non-issue for anyone not living and working in Greece. Our financial system had five years to manage, hedge, and otherwise reduce exposure to a Greek default. Most Greek debt is now held by European governments who can weather these losses. For them it isn’t a big deal because they didn’t enter into these positions expecting a profit, or even their money back. All they were doing is buying stability and time. And given that they delayed the inevitable Greek default by five years, they did a pretty good job. While a few politicians might lose their jobs and damage their legacy over this, the financial system will survive without Greece because of the time they bought us. If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch. Sources: https://en.wikipedia.org/wiki/Economy_of_Greece http://confluenceinvestment.com/assets/docs/2015/daily_Jun_29_2015.pdf http://www.zerohedge.com/news/2015-02-03/who-owns-greek-debt-and-when-it-due http://www.washingtonpost.com/blogs/wonkblog/wp/2015/06/25/europe-strikes-back-it-seems-to-be-trying-to-push-greece-out-of-the-euro/ TheMoneyGeek thanks guest writer Bob Veres for his help writing this post

Leave a comment