The official start of summer was only a few days ago, but the market already feels like it’s taken us on a wild roller coaster ride this year. It certainly makes us feel like we’re in a bear (sideways to down) market, what with the surprising “Brexit” vote in the UK, the dismal first few weeks of the year and increased volatility across the board. So it may come as a surprise that the second quarter of 2016 eked out small positive returns for many of the U.S. market indices, and most of them are showing positive (though hardly exciting) gains over the first half of the year.

The Wilshire 5000 Total Market Index–the broadest measure of U.S. stocks and bonds—was up 2.84% for the quarter, and is now up 3.69% for the first half of the year. The comparable Russell 3000 index gained 1.52% for the quarter and is up 2.20% so far this year.

The Wilshire U.S. Large Cap index gained 2.65% in the second quarter of 2016, putting it at a positive 3.94% since the beginning of January. The Russell 1000 large-cap index provided a 1.44% return over the past quarter, with a gain of 2.34% so far this year, while the widely-quoted S&P 500 index of large company stocks posted a gain of 1.90% in the second quarter, and is up 2.69% for the first half of 2016.

The Wilshire U.S. Mid-Cap index gained 4.33% for the quarter, and is sitting on a positive gain of 6.67% for the year. The Russell Midcap Index is up 1.54% for the quarter, and is sitting on a positive gain of 3.82% for the year.

Small company stocks, as measured by the Wilshire U.S. Small-Cap index, gave investors a 4.09% return during the second quarter, up 4.98% so far this year. The comparable Russell 2000 Small-Cap Index gained 1.96%, erasing gains in the first quarter and posting a 0.41% gain so far this year, while the technology-heavy Nasdaq Composite Index lost 0.56% for the quarter and is down 3.29% for the first half of 2016.

When you look at the global markets, you realize that the U.S. has been a haven of stability in a very messy world. The broad-based EAFE index of companies in developed foreign economies lost 2.64% in dollar terms in the first quarter of the year, and is now down 6.28% for the first half of the year. In aggregate, European Union stocks lost 7.60% in the first half of 2016. Emerging markets stocks of less developed countries, as represented by the EAFE EM index, lost 0.32% for the quarter, but are sitting on gains of 5.03% for the year so far.

Looking over the other investment categories, real estate investments, as measured by the Wilshire U.S. REIT index, was up 5.60% for the second quarter, with a gain of 11.09% for the year. Commodities, as measured by the S&P GSCI index, gained 12.67% of their value in the second quarter, giving the index a 9.86% gain for the year so far. The biggest mover, unsurprisingly, is Brent Crude Oil, which has risen more than 15% in price over the quarter.

Meanwhile, interest rates have stayed low, once again confounding prognosticators who have been expecting significant rate rises for more than half a decade now. The Bloomberg U.S. Corporate Bond Index is yielding 2.88%, while the Bloomberg U.S. Treasury Bond Index is yielding 1.11%. Treasury yields are stuck near the bottom of historical rates; 3-month notes yielded 0.26% at the end of the quarter, while 12-month bonds were yielding just 0.43%. Go out to ten years, and you can get a 1.47% annual coupon yield. Low? Compared with rates abroad, these yields are positively generous. If you’re buying the German Bund 10-year government securities, you’re receiving a guaranteed -0.13% yield (yes, that’s a negative yield). The 5-year yield is actually worse: -0.57%. Japanese government bonds are also yielding -0.3% (2-year) to -0.23% (10-year). Can you imagine paying someone to hold your money for you?

On the first day of July, the Dow, S&P 500 and Nasdaq indices were all higher than they were before the Brexit vote took investors by surprise, which suggests that, yet again, the people who let panic make their decisions, lost money while those who kept their heads in it, sailed through. There will be plenty of other opportunities for panic in a future where terrorism, a continuing mess in the Middle East, a refugee crisis in Europe and premature announcements of the demise of the European Union will deflect attention away from what is actually a decent economic story in the U.S.

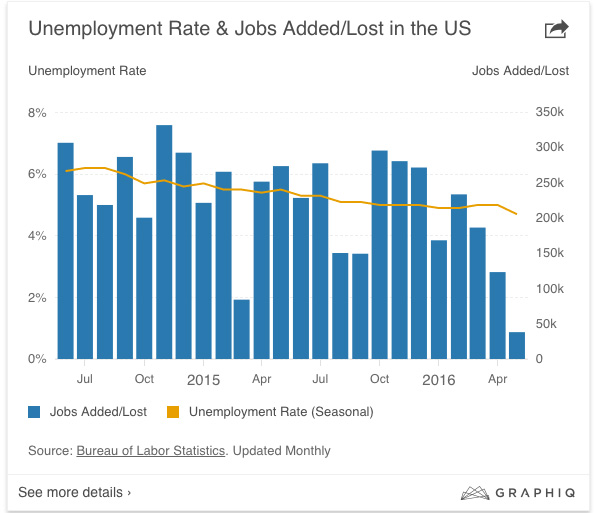

How decent? The American economy is on track to grow at a 2.0% rate this year, which is hardly dramatic, but it is sustainable and not likely to overheat different sectors and lead to a recession. Manufacturing activity is expected to grow 2.6% for the year based on the numbers so far, and the unemployment rate has fallen to 4.7%, which is actually below the Federal Reserve target. Inflation is also low: running around 1.4% this year. The unemployment statistics are almost certainly misleading in the sense that many people are underemployed, and a sizable number of working-age men are no longer participating in the labor force, but for many Americans, there’s work if you want it. Historically low oil prices and high domestic production have lowered the cost of doing business and the cost of living across the American economic landscape.

Despite all this good news, the market is struggling to keep its head above water this year, and is not threatening the record highs set in May of last year. But we’re close, and I suspect that we will challenge and rally above the old highs soon.

Questions remain. The biggest one in many peoples’ minds is: WILL the European Union break up now that its second-largest economy has voted to exit? There is already renewed talk of a Grexit, along with clever names like the dePartugal, the Czechout, the Big Finnish and even discussion about Texas (Texit?) leaving the U.S. How long before we hear about (cue the sarcasm) some localities declaring independence from their states? With active political movements in at least a dozen Eurozone countries agitating for an exit, is it possible that someday we’ll view the UK as the first domino?

A recent report by Thomas Friedman of Geopolitical Futures suggests that the EU, at the very least, is going to have to reform itself, and the vote in Britain could be the wake-up call it needs to make structural changes. The Eurozone has been struggling economically since the common currency was adopted. It is still dealing with the Greek sovereign debt crisis, a potential banking crisis in Italy, economic troubles in Finland, political issues in Poland and, in general, a huge wealth disparity between its northern and southern members. Is it possible that a flood of regulations coming out of Brussels is imposing an added burden on European economies? Should different nations be allowed to manage their policies and economies with greater independence and focus?

Friedman thinks the UK will be just fine, because Europe needs it to be a strong trading partner. Britain is Germany’s third-largest export market and France’s fifth largest. Would it be wise for those countries to stop selling to Britain or impose tariffs on British exports? And more broadly, with the political turmoil in the UK, is it possible that there will be a re-vote, particularly if the European Union decides to make reforms that result in a less-stifling regulatory regime?

You’ll continue to see dire headlines, if not about Brexit or the Middle East, then about China’s debt situation and the Fed either deciding or not deciding to raise rates in the U.S. economy (it won’t). Oil prices are going to bounce around unpredictably. The remarkable thing to notice is that with all the wild headlines we’ve experienced so far, plus the worst start to the year in U.S. market history, the markets are up slightly here in the U.S., and the economy is still growing. The chances of a U.S. recession starting in the next nine months are 10% or less. Yes, your international investments are down right now, but eventually, you can expect them to come to the rescue when the American bull market finally turns.

When will that be? If we knew how to see the future for certain, we would be in a different business. All of us are going to have to resign ourselves to being surprised by whatever the rest of the year brings us, headline by headline. That, however, doesn’t stop me from making my own prognostication about what the market might bring. By the end of the year, I think we’ll see mid-single digit gains for the year, after some hand-wringing over the election, in what I expect to be a rough September and October in the markets. But then again, I thought the Brexit would be voted down, so don’t bet your chips on any predictions anyone has, including me. This keeps us mostly invested with good hedges to absorb whatever volatility the market throws at us.

If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch. We start with a specific assessment of your personal situation. There is no rush and no cookie-cutter approach. Each client is different, and so is your financial plan and investment objectives.

Sources:

Wilshire index data. http://www.wilshire.com/Indexes/calculator/

Russell index data: http://indexcalculator.russell.com/

S&P index data: http://www.standardandpoors.com/indices/sp-500/en/us/?indexId=spusa-500-usduf–p-us-l–

Nasdaq index data: http://quicktake.morningstar.com/Index/IndexCharts.aspx?Symbol=COMP

International indices: http://www.mscibarra.com/products/indices/international_equity_indices/performance.html

Commodities index data: http://us.spindices.com/index-family/commodities/sp-gsci

Treasury market rates: http://www.bloomberg.com/markets/rates-bonds/government-bonds/us/

Aggregate corporate bond rates: https://indices.barcap.com/show?url=Benchmark_Indices/Aggregate/Bond_Indices

Aggregate corporate bond rates: http://www.bloomberg.com/markets/rates-bonds/corporate-bonds/

http://useconomy.about.com/od/criticalssues/a/US-Economic-Outlook.htm

http://www.marketwatch.com/story/first-quarter-us-gdp-raised-to-11-2016-06-28?siteid=bulletrss

The MoneyGeek thanks guest writer Bob Veres for his contribution to this post