One of the areas that regulators have begun to focus on in the investment industry is elder fraud. After hearing about the vicious scams endured by senior citizens, many by their own families, I’ve become more attuned to the clues that a client or relative of mine might be a victim of.

It happens too often: you’ve saved money all your life. Or, maybe you sold your business after investing years of hard work. You’ve chosen the smart path and have a comfortable nest egg as you set sail into retirement. Still, you always have to be on guard! Criminals seek to trick you into willingly handing over your hard-earned savings.

Elder financial exploitation quadrupled from 2013 to 2017, according to the Consumer Financial Protection Bureau. Specifically, these activities originated from unknown scammers, family members, caregivers, or someone in a nursing home. They involved more than $6 billion, with an average loss of $34,200. But in 7% of these instances, losses exceeded $100,000.

In 2017, elder financial exploitation reports totaled 63,500. Sadly, these reports probably represent just a small fraction of actual incidents. According to the FBI, more than 2 million seniors were victimized in the past year. Even former FBI Director William Webster, 95, was targeted in 2014.

Webster was promised $72 million and a new car…if he paid several thousand dollars to cover shipping. Ultimately, the caller was arrested. But not before his relatives in Jamaica had successfully scammed other U.S. citizens out of hundreds of thousands of dollars.

It won’t happen to me

If you’re thinking, “This can’t happen to me,” think again. The best and brightest can fall victim to a seasoned swindler.

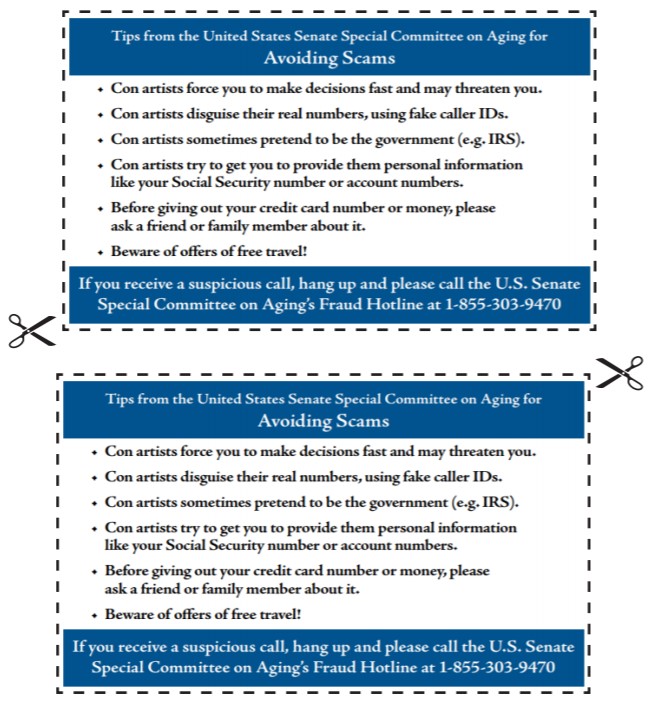

While scams are only limited by the criminal imagination, the U.S. Senate’s Committee on Aging highlighted some of the more common scams in a report entitled “Protecting Older Americans Against Fraud“.

Listed below are the top nine scams. Please familiarize yourself with this list. If you have any questions, we would be happy to talk to you.

- IRS impersonation scams

Scammers impersonating IRS officials claim you owe money and pressure you to settle immediately. If victims make an initial payment, they will often be told that new discrepancies have been found in their tax records, which must be satisfied with another payment.

Don’t fall victim! The IRS will never call you to demand immediate payment. If there is a question about your return, you’ll receive a letter in the mail, not an e-mail, and there is a process to appeal any disputed amount.

- Robocalls and unsolicited phone calls

Robo-dialers can be used to distribute prerecorded messages or connect the person who answers the call with a live person. IRS scammers may use this tactic.

Robocalls often originate overseas, and numbers are usually spoofed (fake) to hide their true identity. Have you recently received a call from someone whose phone number has your prefix? If you don’t recognize the number, it’s likely spoofed and not local.

The FTC has warned not to give out personal information in response to an incoming call. Identity thieves are clever. They often pose as bank representatives, credit card companies, creditors, or government agencies. They hope to convince victims to reveal their account numbers, Social Security numbers, mothers’ maiden names, passwords, and other identifying information. Sometimes all they’re looking for is to record and “steal” your voice imprint, so let them do the talking. Don’t answer any questions with “yes” or “no”, or even give out your name (see 4. below).

Unsure who you are talking to? Just hang up the phone.

- Sweepstakes scams / Jamaican lottery scam

Sweepstakes scams continue to claim senior victims who believe they have won a lottery and need only take a few actions, i.e., sending cash to the con artists in order to obtain their “winnings.”

Sometimes, it’s best not to answer a call if you don’t recognize the number. If it’s a friend, neighbor, relative or colleague, they’ll leave a voicemail message.

- “Can you hear me?” “Are you there?” scams

The goal: get your voice print saying, “Yes.” Then, the scammer charges your credit card using your “Yes.”

If asked, don’t respond. Just hang up. If you get a call, don’t press 1 to speak to a live operator to be removed from the list. If you respond in any way, it will likely lead to more robocalls–and more scams.

- Grandparent scams

“Hi Grandma/Grandpa, guess who?” When you respond, “This sounds like ‘Sally’,” the fraudster will say “she’s” in trouble and needs money to help with an emergency, such as getting out of jail or paying a hospital bill.

If you send cash, expect “her” to call you again, asking for more cash. Victims who were duped later said they had wished they had asked some simple questions that only their true grandchild would know how to answer. Have discussions with your loved ones about what safe word or phrase you might share if they’re really in trouble and need help.

- Computer tech support scam

Whether a computer pop-up screen or an alleged caller from Microsoft, scammers claim your PC is infected with a virus. Please note, Microsoft will never call you to inform you they have detected a virus.

Do not give control of your computer to a third party that calls you out of the blue. Don’t give them your credit card number.

- Romance scams

More and more Americans are taking to the Internet to find a partner. While some find love, others find financial heartache.

Be wary of individuals who claim the romance was destiny or fate. Be cautious if an individual declares his or her love but needs money from you to fund a visit. Or claims cash is unexpectedly needed to cover an emergency. These are huge red flags.

- Identity theft

This was the most common type of consumer complaint in 2016, with nearly 400,000 complaints.

Placing a freeze with the major credit bureaus helps prevent credit cards or loans from being taken out in your name. If you believe you are a victim, call the companies where the fraud occurred, place a fraud alert with the credit bureaus, and file a report with your local police department.

- Government grant scams

In the most common variation of this scam, consumers receive an unsolicited phone call from a con artist claiming he or she is from the “Federal Grants Administration,” or the “Federal Grants Department”–agencies that do not exist. Always remember, grants are made for specific purposes, not because you are a good taxpayer.

Do not wire funds to cover fees for the so-called grant. Government grants never require fees of any kind. If you do, you’ll likely get more requests for additional unforeseen “fees.” If getting a sum of money to someone involves using pay services such as Western Union or going to say Walmart to transmit money, be immediately suspicious.

And, don’t give out bank information or personal information to these swindlers. Scammers pressure people to divulge their bank account information so that they can steal the money in their account. You wouldn’t give bank information to a stranger at the supermarket. You don’t know them. So, why give personal information to someone you don’t know who unexpectedly contacted you?

Always remember, you are in control. When in doubt, hang up. That is how you protect yourself.

If you suspect elder financial abuse, the American Bankers Association suggests the following steps:

- Talk to elderly friends or loved ones. Try to determine what may be happening to their financial situation, such as a new person “helping” them with money management, or a relative using cards or credit without their permission.

- Report the elder financial abuse to their bank. Enlist their banker’s help to stop it and prevent its recurrence.

- Contact Adult Protective Services in your town or state for help. Report all instances of elder financial abuse to your local police—if fraud is involved, they should investigate.

Be on alert

At the end of this article, there is a list of useful tips that you can print. Place it near your phone. These cards can be a useful tool to help protect you against swindlers.

Final thoughts

Our mission is to help you reach your financial goals. We are proactive in our recommendations. But sometimes, a good defense is the best offense. It’s heartbreaking to hear stories of theft. We don’t want you to become a victim and another government statistic.

If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch. We start with a specific assessment of your personal situation. There is no rush and no cookie-cutter approach. Each client is different, and so is your financial plan and investment objectives.