Many investors will be glad to finally see the end of the third quarter of 2015, and most of them will feel like their portfolios are worse off than they actually are. That whooshing sound you hear is not just air being let out of the markets; it’s also an end to that optimistic feeling that many people had been cautiously building during the long 6-year bull market that followed the Great Recession.

The past three months turned yearly gains into yearly losses almost completely across the board of the investment opportunity set. The Wilshire 5000–the broadest measure of U.S. stocks—fell 6.91% in the third quarter of 2015, posting a total return of -5.79% in the first half of the year. The comparable Russell 3000 index is down 5.45% so far this year.

The Wilshire U.S. Large Cap index dropped 6.44% of its value for the quarter, and is now down 5.15% for 2015. The Russell 1000 large-cap index is down 5.24% so far this year, while the widely-quoted S&P 500 index of large company stocks posted a loss of 6.94% in the third quarter, and is now down 6.75% for the year.

The Wilshire U.S. Mid-Cap index lost 8.96% for the quarter, and is now off 4.86% as we head into the fourth quarter. The Russell Midcap Index has lost 8.58% so far this year.

Small company stocks, as measured by the Wilshire U.S. Small-Cap index, gave investors a 10.88% loss during the latest three months, which takes the index down 7.29% so far in 2015. The comparable Russell 2000 Small-Cap Index is down 7.73% in the first three-quarters of the year, while the technology-heavy Nasdaq Composite Index lost 7.35% for the quarter, and stands at a 2.45% loss for the first three quarters of the year.

Meanwhile, in the global markets, the broad-based EAFE index of companies in developed foreign economies lost 10.75% in dollar terms in the third quarter of the year, for a negative 7.35% return so far this year. In aggregate, European stocks lost 9.07%, and are down 7.33% for the year. Emerging markets stocks of less developed countries, as represented by the EAFE EM index, were down a whopping 18.53% for the quarter, and are down 17.18% for the year.

Looking over the other investment categories, real estate investments, as measured by the Wilshire U.S. REIT index, gained 2.88% for the third quarter, but is still standing at a 3.01% loss for the year. Commodities, as measured by the S&P GSCI index, lost 19.3% in the third quarter, largely due to a fall in oil prices that may be nearing its end. They are down 19.46% this year.

There were many contributors to the loss of confidence in the stock market, and they appear to have been mainly psychological. Analysts blame the Federal Reserve Board for not having raised rates as the so-called “smart money” seems to have expected in September. Why are low rates a bad thing? Because Fed economists seem to believe that the economy has not recovered sufficiently to warrant stopping the central bank’s long-running stimulus program. Who are we investors to argue with the Fed economists?

Except… The explanation for not raising rates had little to do with actual economic activity, which is finally moving ahead, as of the second quarter, at an annualized 3.9% growth rate for U.S. GDP. This is higher than the 3.7% estimate from the Bureau of Economic Analysis, and much higher than the 2% rate that the U.S. economy has experienced since 2009. At the same time, consumer income, wages and salaries, and spending are all increasing modestly, existing home sales are growing at a 6.2% rate over last year, and the unemployment rate, once higher than 10%, has finally dropped down to the 5% range.

The Fed explained that it was delaying its rate rise because the core inflation rate—currently 1.83%, is below the 2% target rate the Fed set back in June 2012. Some people believe low inflation is a GOOD thing, and speculate that’s the real reason.

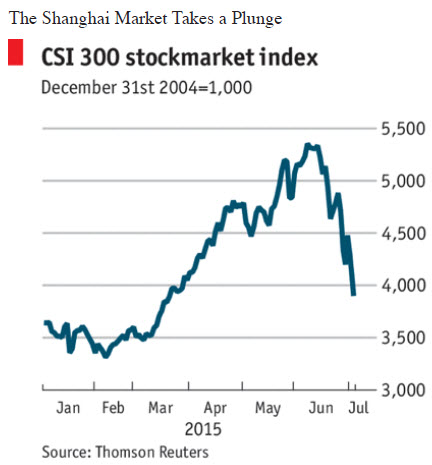

And another reason why many investors are nervous about the markets—could be the slower growth of the Chinese economy, coupled with the recent unnerving drop in its stock market. Unfortunately, the Chinese government controls the economic statistics that come out of the world’s second largest economy, which makes it hard to know exactly how fast China is or isn’t growing. But it’s worth noting that Chinese stock prices, even after the drop, are still up 31.6% from where they were a year ago.

For the time being, investors will have to continue to accept interest rates at historically low levels. The Bloomberg U.S. Corporate Bond Index now has an effective yield of 3.42%. 30-year Treasuries are yielding 2.87%, down from 3.13% a quarter ago, and 10-year Treasuries currently yield 2.06%, down from 2.36% in June.

At the low end, the yield on 3-month U.S. T-bills remains at 0.01%. 6-month bills are only slightly more generous, at 0.08%. Long-term (30-year) municipal bonds are yielding 3.16%, more than comparable Treasuries, and you get the federal tax-exemption thrown in for good measure.

When you look at the decline year-to-date, you see relatively small losses. But many investors are remembering that they were 10-15% wealthier just a couple of months ago, measuring their pain from the high point of the various indices. It’s tough to watch your portfolio go down, but it’s also worth remembering that people have been predicting a significant downturn—erroneously—for the better part of six years. Now that the downturn has finally arrived, it hasn’t been terribly painful, mostly giving back gains that were posted in the first two quarters.

The third quarter could be a temporary drawdown that sets the market up for a push back into positive territory by the end of the year, which would give us a record seven years of positive market performance. Or we could see the year end in negative territory, perhaps even giving us the first true bear market (defined as a drop of 20% from the peak) since the Great Recession. We don’t know how the psychology of millions of investors will turn in the next few months, and neither do the smart money analysts who thought that interest rates would be nudged upward by our central bank last month.

We do, however, have confidence that the next bear market will be followed by yet another bullish period that will eventually take us back into record territory, and we’re pretty sure that the markets will punish anyone who tries to outguess their unpredictable behavior in the short term. If you know what the next quarter will bring, please tell us now. Meanwhile, perhaps we should celebrate the fact that we can buy many kinds of investments at cheaper prices than we could just three short months ago. It’s not much, but it’s something to feel good about.

In our client portfolios, our returns this quarter were buffered by a larger than normal cash position, investments in inverse funds, a focus on defensive sectors, and by selling call options against some of our positions. If the market chooses to launch a 4th quarter rally, we’ll be ready for it. It may even have already started. But if the market instead chooses to go the bear route, we’ll increase our defensiveness further.

If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch.

Sources:

Wilshire index data: http://www.wilshire.com/Indexes/calculator/

Russell index data: http://www.russell.com/indexes/data/daily_total_returns_us.asp

S&P index data: http://www.standardandpoors.com/indices/sp-500/en/us/?indexId=spusa-500-usduf–p-us-l–

http://www.tradingeconomics.com/united-states/unemployment-rate

Nasdaq index data: http://quicktake.morningstar.com/Index/IndexCharts.aspx?Symbol=COMP

International indices: http://www.mscibarra.com/products/indices/international_equity_indices/performance.html

Commodities index data: http://us.spindices.com/index-family/commodities/sp-gsci

Treasury market rates: http://www.bloomberg.com/markets/rates-bonds/government-bonds/us/

Aggregate corporate bond rates: https://indices.barcap.com/show?url=Benchmark_Indices/Aggregate/Bond_Indices

Aggregate corporate bond rates: http://www.bloomberg.com/markets/rates-bonds/corporate-bonds/

Muni rates: https://indices.barcap.com/show?url=Benchmark_Indices/Aggregate/Bond_Indices

http://money.cnn.com/2015/06/29/investing/china-stocks-bear-market/index.html

http://www.reuters.com/article/2015/10/01/us-usa-economy-idUSKCN0RV4I120151001

http://www.theguardian.com/business/2015/sep/28/us-stock-markets-fall-concerns-china-economy

The MoneyGeek thanks guest writer Bob Veres for his contribution to this post.